…to me anyway. Today, I gave the keynote for the launch of Lloyds Banking Group’s Consumer Digital Index 2017, where I talked about the importance of improving digital skills for the people who are most excluded in our society and how we can all be part of that solution by working together across sectors. One big piece of news to come out of the launch was that in the past year, 1.1 million more people in the UK now have the five basic digital skills they need to thrive in our digital society. This means that the 12.6 million that I’m always talking about has gone down to 11.5 million.

Of course this is still a considerable amount of people but it’s great news as it certainly means we’re moving in the right direction.

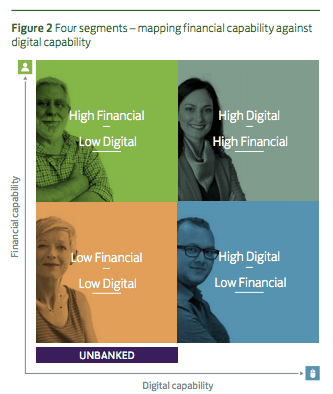

Image courtesy of Lloyds Banking Group’s Consumer Digital Index 2017

#DigitalIndex17

This is the second Consumer Digital Index that has been compiled by Lloyds Banking Group and it is a valuable resource for the tech industry, providing a unique view of, not only the digital capability, but the financial capability of the UK population.

This year’s Index has the addition of a ‘Basic Digital Skills measure’ which paints a clear picture of the state of our digital nation. The measure is designed by digital skills charity Doteveryone and looks at the five skills which help people make the most of the internet: managing information, transacting online, communicating, problem solving and creating.

Of course, the main focus on the Index is on money and financial capability, so it also contains the new addition of quantitative research from the financial inclusion charity Toynbee Hall, in order to paint a clearer picture of those who don’t have a bank account and their financial and digital needs. FYI, the number of UK adults who do not have a bank account is 1.71m.

Key findings

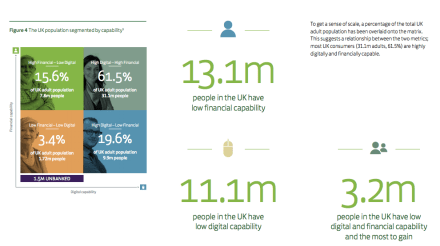

One of the main findings is that the 63% of people who do not have a bank account but who do have a smartphone cope fairly, or sometimes, well with money, however there are still 16.2m people who need more support with financial education.

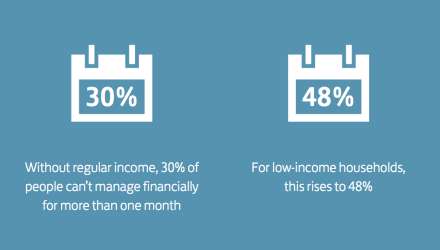

Financial resilience is a big problem for a lot of people in the UK. The Index has found that without their regular income, 30% of people wouldn’t be able to manage financially for more than a month – this rises to 48% for low income households.

Image courtesy of Lloyds Banking Group’s Consumer Digital Index 2017

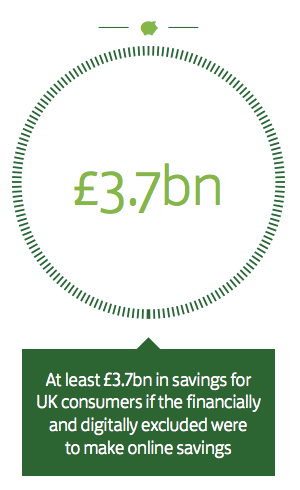

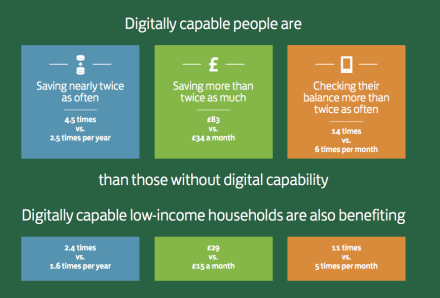

In terms of savings, digital can help. The Index has found that digitally capable people are saving more than twice as much as those who are not and the average amount that people can save per year by using discount and cashback websites is £444 – a massive saving. It also found that 67% of people have used online banking to help avoid paying overdraft fees.

Image courtesy of Lloyds Banking Group’s Consumer Digital Index 2017

Digital Motivation

Despite the fact that there are now 1.1 million more people in the UK with digital skills, there are still challenges in motivating the people who have never used the internet (the “offline”). Motivation is very important, because without it, people simply won’t do it.

68% of the offline population actually said that nothing could motivate them to get online but 45% of people said they turn to friends and family to learn how to use the internet.

Image courtesy of Lloyds Banking Group’s Consumer Digital Index 2017

In Online Centres across the UK, staff and volunteers are motivating people to get online. Whether that’s by tailoring devices to their needs, piquing their interest by showing them videos of their favourite music artists on YouTube or showing someone whose family lives abroad that they can speak with them via Skype. It’s all about engagement and once they’ve found that spark, more often than not, it’s followed by a roaring fire.

Powerful recommendations

One of the recommendations in the Index states that ‘the best way to increase the pace of change in the level of financial and digital skills’ is with direct dialogue, either through face-to-face support or peer-to-peer guidance. I am very much on board with this. Good Things Foundation works with over 5,000 local centres across the UK – the Online Centres Network. We’re a big club with a shared vision; a social movement and every day the volunteers and tutors in these centres help people, like Daniel Blake (from the film “I, Daniel Blake”). They are genuine trusted faces in very local places, reaching those most in need.

Another recommendation is to widen the conversation – according to the Index 43% of people don’t know where to go for help to learn digital skills. To reach this 43%, it’s more important than ever for us all to work together. For example, Lloyds Banking Group staff can point their customers towards their local Online Centre to gain help.

On the panel with Leigh Smyth and Sarah Porretta from Lloyds Banking Group, Sian Williams from Toynbee Hall and Karen Price from the Tech Partnerhship

I was delighted that we were a partner in reviewing and advising on the Index, and I was also delighted to be given the opportunity to speak at the launch. Lloyds Banking Group is a great partner of ours and they really do get it. They get that helping people to be digitally included helps people to have a better life, and it’s better for society, and for the bank too. They are exemplar partners, embedding digital inclusion right across their banking divisions.

Final musings

Everybody can help – Government, big companies, small organisations, individuals – but we need to do this quicker. We can all do more, everyone including Lloyds and Good Things Foundation and the Online Centres Network. If we all work harder as well as better together, we can make sure everyone everywhere is on the same page and we’ll be able to achieve so much more – even if it’s simply pointing digitally challenged friends or family towards their local Online Centre.

At next year’s Digital Index launch, we don’t want to be celebrating another 1 million people helped – we want to be celebrating 2 million, 3 million, 4 million more.

As Nick Williams from Lloyds Banking Group said: “We shouldn’t give up, we can’t give up, we won’t give up.”