Last week I attended a sneak preview event of Lloyds Bank’s Consumer Digital Index – officially launched on Saturday – and a Lloyds/Demos roundtable event afterwards to discuss the important role of technology and digital in financial inclusion. I already knew that there was a close correlation between the two but this Digital Index backs it up, with robust figures taken from a research sample of 1 million Lloyds customers – the largest study of financial and digital capability ever conducted in the UK.

A lot people who are financially excluded are the same people who find themselves digitally excluded as well – people on a low incomes, with disabilities, and older people for example. It’s the link between digital and financial exclusion – particularly for this demographic aspect – that I’m really interested in.

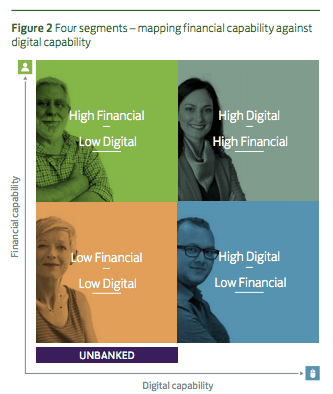

The report maps financial capability against digital capability. Ideally, we want to reach the ‘unbanked’ [Source: Consumer Digital Index 2016, Lloyds Bank]

Tinder Foundation and our network of community partners are working towards a shared vision – to help people be capable to use the internet in a way that’s purposeful and beneficial to each of them. The majority of people who don’t use the internet are on low incomes, and financial capability is clearly essential for them. For people on low incomes, saving money by being online will help them in the long run, with consumers on the lowest income making average savings of £516 per year. We know that some people don’t use the internet because they can’t afford to buy equipment or afford broadband. People financially benefit by being online, but they lack the money to invest in getting online in the first place. It’s very much a chicken and egg scenario. I don’t know the solution (yet!) but we need to come up with something to break the cycle.

The stats

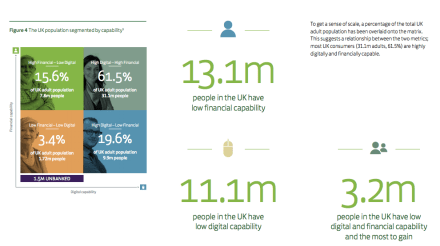

Being a big stats nerd, my favourite part of the Consumer Digital Index was the numbers. It’s encouraging to see that 31.1 million adults have high digital and high financial capability, but there’s still a disappointing 13.1 million people with low financial capability and 11.1 million with low digital capability. According to the Index, this works out as 3.2 million people in the UK today who have low digital AND financial capability. That’s 3.2 million people who are missing out on all the benefits, both financial and otherwise, that the internet can bring.

[Source: Consumer Digital Index 2016, Lloyds Bank]

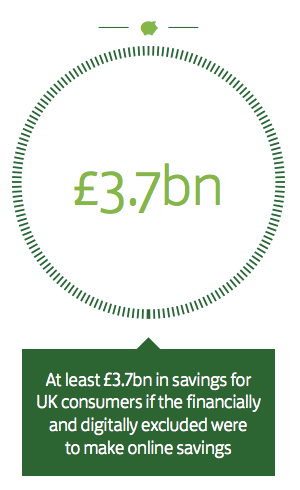

The Index says that if the financially and digitally excluded were to turn it all around and start to do more online, the benefit would be £3.7bn in savings for UK consumers. Savings are great, as are the other financial benefits that being online can bring. Being online means you can have access to debt advice and info from services like the Citizens Advice Bureau, for example.

[Source: Consumer Digital Index 2016, Lloyds Bank]

I understand that not everyone wants to do things online. Nick Williams, Consumer Digital Director of Lloyds Banking Group, said they have 24 million customers and only 11 million actually do their banking online.

One element of the Index that I found to be particularly useful was ‘The four elements of financial wellbeing’. Focussing on ‘Security’ and ‘Freedom of choice’ it looks at where consumers would be if they became financially included now and where this will lead them in the future. I have included the table below. As you can see there are both present and future benefits to choosing to be financially included and it would be unwise to ignore them.

[Source: Consumer Digital Index 2016, Lloyds Bank]

When writing about the Index, a lot of the media have focussed on the amount of money people can save by being online. It’s definitely a motivator if even consumers on the lowest income can make average savings of £516 per year. Let’s go back to the ‘poverty conundrum’; the intractable challenge for people on low incomes. We need to make sure that they can afford the internet in order to make those savings. What we need to do is create a behaviour change, where people have the ability to get online and be in control of their finances now and be prepared for what they might need in the future; where people have the financial freedom now to enjoy life and be on track to meet their financial goals in the future.

This is the 21st century. Today, digital underpins almost everything. Here’s the punchline. We’re determined to reduce the number of people without basic digital skills as much as possible; that’s the day-job. We’ve got a goal to help more than one million people between now and 2020. What the sectors should be doing is working together as much as possible to help both fronts – financial and digital. Of course, you can create better financial capability without digital, but why would you? There are so many benefits for consumers when we make sure they go hand-in-hand.